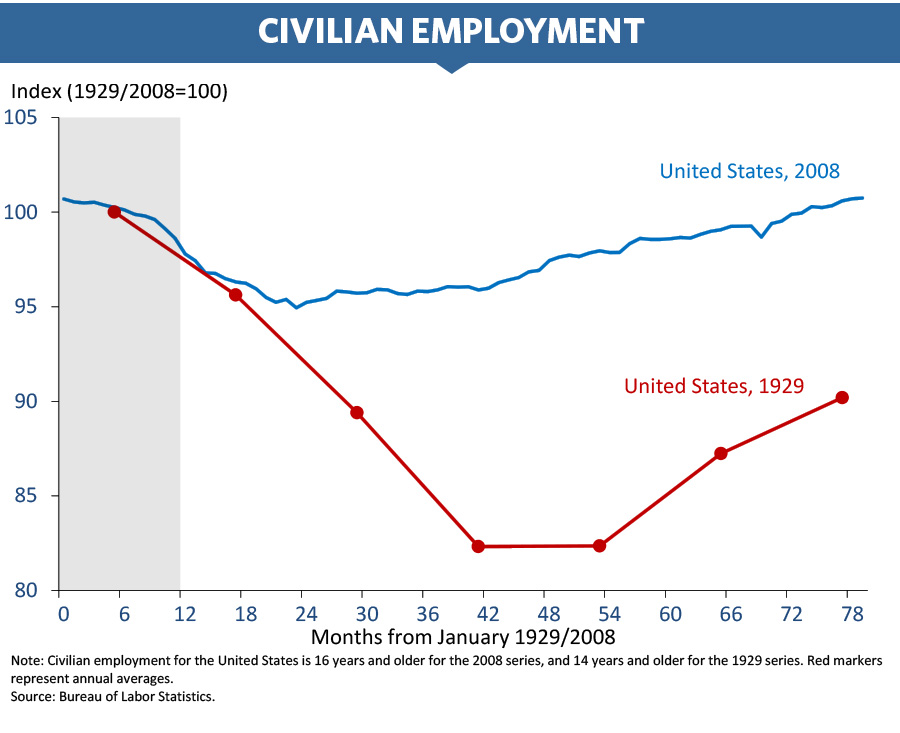

I also think it's interesting that the 2008 mortgage crisis was very close to becoming just as bad as the great depression, but fiscal policy prevented that.

It's easiest to see this in side by side charts. The magnitude of stock market losses and economic data was tracking almost exactly with the great depression, until the central banks intervened.

> I also think it's interesting that the 2008 mortgage crisis was very close to becoming just as bad as the great depression, but fiscal policy prevented that.

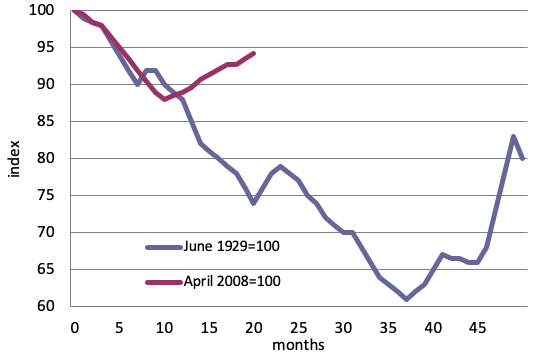

Compare unemployment in the Great Depression vs Great Recession:

Fiscal policy certainly did help, but the Great Recession probably would have still been significantly smaller than the Great Depression for several reasons.

(I suspect the Great Recession is more analogous to the Long Depression of the late 19th century, in that both of them significantly worsened inequality, while the Great Depression reduced inequality. I suspect whenever the US starts dealing with its mountain of debt, the resulting recession/panic/depression will also reduce inequality, though I doubt too many people will be cheering that when it happens).

> Compare unemployment in the Great Depression vs Great Recession:

The second chart I linked does exactly that. The point is to not look at the absolute numbers because, the unemployment trend in 2008 was reversed by fiscal policy, but during the great depression there was no such intervention.

Until the central banks intervened, unemployment was tracking almost exactly with the great depression.

You also can't compare the absolute unemployment numbers for a lot of other reasons. A major one is that unemployment (The U6 number, i.e. "real unemployment") in the first half of the century was consistently 10%+ higher than it is today. That's because of less women in the workforce.

In 1929, the workforce was considered fully employed with an unemployment rate (U6) of 15%. In 2008, we considered a fully employed workforce to be just 5% unemployment.

The feature that stands out the most to me is that the black "boom or bust" line that shows prosperity/recession is effectively never at 100. It crosses the line (going up or down) a bunch of times, but is almost never on the line. I have to wonder if more balance with this would result in better outcomes, or worse.

Also, and this is just an eyeball analysis from the pdf, the booms seem roughly balanced with the busts until the great depression. The prosperity of WWI seems to have set up the cycle of bust for the great depression.

> I have to wonder if more balance with this would result in better outcomes, or worse.

Iirc that is exactly the problem that the Soviets claimed they solved with state-owned and centrally planned production, no more boom/bust cycle. And early on it did have some in the West worried about it. Turned out not to work, probably b/c you can't stablize an inherently unstable complex system.

Fundamentally centralized control has an information problem. Decisions about how to allocate resources require complex information that mostly exists at the edge, but communicating all of that back to the central controller would just overwhelm them. This is why markets work so well, the decisions about how to allocate the resources are pushed down to where the information is. But this is also why market are bad at solving systematic issues, in that case the information is above where the decisions are being made. You can see where there are tradeoffs and cases where one system works better than the other, so anybody who issues a blanket statement like "markets are always the best solution" is not operating with a complete picture of the world.

I seem to remember that due to political infighting and ass-covering, they never really tried it. There were competing proposals that they hybridized in broken ways, and nobody in power wanted to commit to have their name on something that might fail or become unpopular.

I recommend the excellent novelization of the period “Red Plenty”. My understanding is that it stays fairly true to the history.

> I seem to remember that due to political infighting and ass-covering, they never really tried it.

What do you mean by "never really tried it"? This was a state that set production quotas, dictated prices, and set priorities in 5 year intervals. What more could they have done? The fact that even a regime that was willing to starve and enslave its own people could not make a planned economy work, just shows the futility of the approach.

I think the commenter was referring to a supposedly accurate historical fiction book that describes how the system was never truly working in an honest fashion. I have a colleague that worked in optimization in the Soviet Union and he explained that factories would lie about their data in order to look better and essentially you'd have garbage in and garbage out for the models. So we don't know if the linear programming tools were truly broken or if it was because all the input data was corrupted. I think the book said the same thing.

Like you, I've become fairly suspicious of economic models that attempt to explain something complex and unstable like an economy. Equilibrium is an exception in the real world...not an inevitability and the caveats of that model are often discarded.

The point is not about the basic principles, but how these decisions were made. This is like being a higher up in a company making a call about something, which goes from placing the bet on the wrong horse, political infighting between different departments, up to decisions which are based on incentives that go counter to the well-being of the company. We are talking about humans with all their flaws.

Especially large corpos developed more and more similarities to how eastern bloc countries were operated, believe it or not. Very top down decision making (with all the problems), large bureaucracies, people who are employed but effectively don't do anything ("bullshit jobs" / David Graeber), company propaganda (all hail to the great company!), bothersome people getting "mistreated", and so on. I've experienced the eastern bloc from inside and I'm not sure whether I should laugh about or be terribly afraid of the things that are still to come.

Edit: Forgot one big thing: Metrics / quotas.

The other thing to keep in mind that "responsibilities" were split between members of the eastern bloc and the decisions who took over what that were often influenced by all kinds of things, just not what made most sense.

There was also huge trade embargo, CoCom, in place.

> The fact that even a regime that was willing to starve and enslave its own people could not make a planned economy work, just shows the futility of the approach.

I disagree with this way of thinking. A willingness to apply lots of cruelty to an attempt doesn’t make up for a lack of skill or capabilities. Cruelty is often a failure-mode, not a recipe for success.

>What do you mean by "never really tried it"? This was a state that set production quotas, dictated prices, and set priorities in 5 year intervals. What more could they have done?

Obviously: not have different political factions and concerns from individual officials to "look good" affect the content of those plans, nor have the same factions and concerns distort the reports about the state of production and the results of said plans.

And instead to try what they purported to be doing but didn't do: plan solely based on optimization concerns, and get back non purposefully-distorted reports so that they can re-plan and course-correct as needed.

Btw, those "five year plans" are not what people think, which usually involves a mental picture of someone calculating the amount of desired production of X or Y product for the next five years and setting some prices in stone.

They rather were sets of goals and associated organized efforts on multiple fronts to meet them. Like "let's industrialize that province" or "let's build transport infrastructure", etc.

Like current multi-year "initiatives" or often still call "plans" like "The Biden- Harris Plan to Revitalize American Manufacturing and Secure Critical Supply Chains in 2022"

I think it's much simpler than that. Instead of factories self-reporting, you have rivals report on each other, as well as client and suppliers report on what went in and out of the factory in a given time period.

It wouldn't be a perfect system, but like capitalism the competition would force everyone into relative honesty. It is pretty weird they didn't do that at the time though, considering the KGB kinda had that sort of setup with respect to everyone individually being required to snitch on each other.

The best critique I heard about the central planning system is that it’s just that, planning.

You might be able to plan, but what about the advancements that nobody would plan for.

“Don’t build a faster horse”

Would a communist system ever advance beyond the planned scientific and enginnering goals? Is there someone thinking “what people need doesn’t exist?” and actually direct resources to it?

That’s the beauty of the the free market system - you can come up with a crazy idea and just do it. You often fail, but if you succeed, the risk you took is rewarded.

I can’t ever see a communist system coming up with an iPhone. They might copy an existing product, but that’s not innovation.

> I can’t ever see a communist system coming up with an iPhone.

Soviets invented a lot of things, in terms of aviation, computers, celestial navigation in intercontinental missiles. There was also an article, which I read recently but failed to find it now, about how they revolutionized mechanical watches, and came out with their own quartz movements, without copying anyone.

Oh lastly, they did the "iPhone of sea going vehicles", the erkanoplan, and VLIW computing which led us to Itanium at some point [0].

Soviet citizens were always at the mercy of central planners deciding if they got to enjoy any innovations (mostly aped from the west). Toasters only started production in 1967 and were mostly unobtanium for the next 25 years.

While the title is provocatively titled, "How the Soviets revolutionized wristwatches", it seems to be more of a play on words around the Soviet revolution. The article is about how they bought watchmaking equipment from the US, looted machinery from Germany after WWII, and copied swiss designs.

Soviet watches were workhorses, but not revolutionary at all.

>You might be able to plan, but what about the advancements that nobody would plan for

You obviously adjust the plan? Planning was never supposed to be some static system (and the "5 year plans" are not about market planning, they were more like "5 year initiatives to improve this or that aspect", e.g. "develop more tank making capacity", or "take a man to the moon").

>I can’t ever see a communist system coming up with an iPhone.

The water surface in the ocean is almost never at "sea level".

Markets are a chaotic system.

> the booms seem roughly balanced with the busts until the great depression

Yup. Like waves in the ocean!

> The prosperity of WWI seems to have set up the cycle of bust for the great depression.

The setup was to peg the dollar exchange rate with gold, and then inflate the money. Such "pegging" historically has always led to a massive correction.

> The water surface in the ocean is almost never at "sea level".

> Markets are a chaotic system.

Don't blame the boom-and-bust in the US on markets. Their heavy-handed policies make them especially crisis prone. Their northern neighbour of Canada had much smoother sailing, thanks largely to a more laissez-faire approach to banking.

How do you meaningfully compare a tiny economy like Canada’s to the 800 lb gorilla of the USA, the global military and economic superpower whose currency rules the world which is conservatively ten times larger than Canada and doesn’t need/act to police the global dollar trade?

In the relevant time period, the US was not the global hegemon, and there was no global dollar trade.

Also a lot of the policy mistake in the US were made at the state level, and that is comparable in scale with Canada.

In any case, it's easy to compare different economies, as long as you are careful what you are doing. And, if anything, overseas demand for your currency should make it easier to run your monetary and financial system.

> I have to wonder if more balance with this would result in better outcomes, or worse.

After reading Taleb, these "boom or bust" cycles are a feature not a bug. My own simplified interpretation: You need booms to fund moonshot ideas and busts to get rid of ideas that don't work. Also a bit similar to neural network training. You first pump in all kinds of information and then aggressively prune to get rid of mostly bad information.

They don't always all line up in time. Companies grow and die all the time.

Trends, Hypes and Bubbles are probably a consequence of human nature: most investors have a deep fear-of-missing out, so in general money loves to jump on the hype-train. Likewise, fear and uncertainty easily spread: markets moving together. When a couple of businesses fail, that insolvency or illiquidity spreads to related businesses.

Booms and busts have cyclic effects. Booms provide more capital and credit that can be reinvested and beget more booms; busts collapse demand and can contagiously bust other sectors.

The responses to your observation are hilarious. They'd have you think that the mass hiring by FAANG in 2021 and early 2022 followed by layoffs was a good thing. You accurately observe it as being screwy, which it is, but people are brainwashed into thinking it isn't - or is even a good thing.

I'm trying to figure what the black "boom or bust" line actually is mathematically speaking. It looks a bit like they've run a regression on GDP and show the deviation above or below trend? Maybe it's in the text? Trying to figure it.

It took me a few looks to figure this out, but out of all the various y axes on this chart, this appears to correspond to "business volume scale," which is exactly 0 on the flat line. The axis itself is found under the years 1845, 1895, and 1930.

What "business volume scale" means or how it is measured, however, I don't see specified anywhere, and after an admittedly cursory web search plus FRASER search of 20 minutes or so, I can't figure it out. The text blurb for "business activity" seems to mean it is probably some aggregation of industrial production and consumer spending, but what 0 is indexed to and what the deviations mean is less clear.

Stability will beget over-confidence which will bring exuberance. If the system feeds on its own information it might be impossible to stabilize.

And do you even want stability? The boom cycle produces exuberance that allows funding risky projects of which a small number become smashing success. The bust destroys the rest of risky project, which allows recycling of labor and resources. Arguably this is a better model for economic advancement, compared to a steady state where stagnating businesses continue to stagnate, hoarding resources in under-productive pursuits.

I kind of wish the scale would go out further into history; I'm not sure if something like that exists (maybe for someplace like England or China?). I also would like to see it replicated for different areas of the world, as well as how the trends correlate with one another over time.

The period since the industrial revolution has been anomalous in many respects in terms of population dynamics and public health, and I imagine it would show up somehow in economic trends? On the other hand going back further in time I assume it becomes increasingly difficult to scale things on some common metric.

The miscalculation was than allies didn't do a parade in Berlin. This way Germans didn't understand how hard they lost WWI, so reparations seemed unfair. That mistake wasn't repeated on WWII.

However hard they lost, repearations would still seem unfair. They still thought their treatment unfair after WWII and all that parading - it took a decade of "training" to convince the Germans that they were the baddies in WWII (and a hell of a lot were never convinced).

Besides the WWI loss they quickly attributed to "internal traitors" (Jews and leftists in general). Parades wouldn't change that.

>If reparations were seen as a fee for remaining independent country they could be very fair given the alternative.

That would be an ever greater insult. Instead of merely unfair, they'd be seen as both unfair and insulting - and threatening ("Our independency is at their mercy? Fuck them at the first opportunity we get!").

That level of insult seemed to work perfectly for Germany and Japan after WW2. Look how polite they are after occupation and giving away half of the country to Russians.

Well, they didn't really give anything away voluntarily.

They lost a war, and got to suffer that as a consequence under postWW2 arrangments (and that was the light option, more like a slap on the wrist: they were also plans to fully deindustrialize and starve them to death https://en.wikipedia.org/wiki/Morgenthau_Plan ).

And they're building up a liking to fascism and national arrogance again in the last few decades. The Japanese too - which never repented for their attrocities to China either.

The difference between the first and second, is that after the second, the ‘Axis’ states were brought into the global economy. Germany and Japan became famously successful both financially and technologically. The economic growth wasn’t to be sustained in the long run, but it intwined them with global markets. Globalization is arguably the biggest force for peace in the western world, save for nuclear deterrent.

The Treaty of Versailles main problem was that it wasn't really crippling enough to destroy Germany but still enough to hurt. But most of that was at the chaotic early years of the Weimar Republic, which by the 1920s had stabilized the situation with American loans.

It was the effects of the Great Depression and internal politicking that gave power to Hitler. The Nazis hatred wasn't directed to the West that enacted that treaty, it was to the east for the Communists and the "subhuman" minorities.

Germany defaulted on some of the payments and France responded to that by occupying Ruhr (https://en.wikipedia.org/wiki/Occupation_of_the_Ruhr). That took out a substantial portion of Germany's production capacity, but they were mandated to keep paying the reparations. The German state tried to keep up with that by printing money, triggering hyperinflation and paving way to the Nazi regime.

When you combine that with Germany and Prussia's lack of access to steel it meant nobody could make anything whatsoever. The impact of not being able to import steel and French occupation of the one major remaining steelworks plant in Krupp is one of the handful of reasons why Prussia was dissolved and absorbed into the greater Weimar Republic nine years later. Prussia couldn't handle the debt caused from the two years of no steel and coal at a time where the republic was so poor they were asking the English and Americans for loans they knew they couldn't repay.

You've got the dates mixed up. The era of hyperinflation and the occupation of the Ruhr occurred from 1921 to 1925, after which the "Weimar Golden years" occurred where the NSDAP were a small minority. The Great Depression occurred in 1929, which promptly crashed the German Economy. Unlike in 1921, this time the government chose austerity which caused great hardship and radicalized much into either the NSADP or KPD. The ruling centrists weren't able to govern without support of either, hence they planned to use Hitler as a "puppet" between the President and the Vice Minister. That plan backfired, although it is to note Hindenburg could have fired Hitler at any time.

Afaik, the printed money to continue paying all the wages for the workers in the occupied area, who went on strike, due to the occupation. Don't think they could pay reparations with freshly printed Reichsmark.

Hitler had insisted on meeting in the exactly same rail car, within which the German surrender of WW1 had been signed, to have the French sign their surrender in WW2. If that's not a sign of hate, I don't know what is.

This was more of a gesture towards the aristocracy that was still heavily present in the Army. For some context, the french also insisted that the 1919 Treaty of Versailles was signed in the same place as the 1871 Treaty of Versailles (which was similarly harsh).

I sorta kinda agree. The US should really have returned to isolationism after WWII instead of allying with Western Europe in conspicuous opposition to the USSR. On the other hand, the efforts of the USSR to agitate for communist revolutions in other countries made Western Europe – with weakening influence over its colonies – very nervous.

But if Russia really wants to stop being a pariah it can just give up its childish posturing, remove its troops from Ukraine and open up its economy, to the benefit of its own people. Sanctions aren’t reparations

Maybe you missed it, but reparations are already being enacted. Just today the EU approved giving Ukraine $3B that Russia's assets deposited in Europe earned this year. And there are talks about giving Ukraine loans that Russia must then repay.

Media murmuring isn't anything legally binding. Russia have plenty of leverage to sue for peace. Namely that this is a war of attrition and Russia has plenty of cannon fodder, exhausting Ukraine in the long run. If it means no more lives lost and the territory returns to pre-war borders, Ukraine would certainly sign without issuing debt.

But the Russian leadership has decided that it wants to usurp territory and be the villian, in full understanding of the consequences. After WWI, Germany had to pay ~550 billion dollars after being turned to rubble. That amount compounded with the depression generated enough unrest and bitterness to give Hitler a willing audience.

They always start with the murmurs to prepare public opinion.

And in any case, I think people really are failing to see the equivalence here, and it's scary. The suggestions to "just stop" (translation: "just lose") are actually serious. You'll have an economically crippled Russia with a wounded collective ego. Perfect setup for a rematch. Just like WW1 to WW2. But the normalizers have the majority opinion on their side at this point, and sadly nobody will stop them from making this tragedy a reality.

So: there really is an equivalence here, and sadly history teaches people nothing. This time they are right, dammit. With any luck, our grandkids will live to discuss how this was the biggest geopolitical miscalculation.

Don't think I have a point? Think about how everyone expected Russians to take to the streets and overthrow Putin back in 2022. The level of delusion is unreal.

> The suggestions to "just stop" (translation: "just lose") are actually serious.

Lose? You mean retreat to their own pre-war borders? To lose would be if they actually had to pay reparations or lost territory of their own. As I said, this would not be how the negotiations play out as Russia has the numbers to keep the war going as long as it wants.

But sure. Tell me what would be lost in Russia ending the war?

> Think about how everyone expected Russians to take to the streets and overthrow Putin back in 2022.

Who is going to try and overthrow the leader who disappears people? Everyone saw what happened to Prigozhin when he dissented. And of course, there are plenty of pro-war nationalists that would take Putin's place should he ever die. So I'm not sure what point you're trying to make here, or how it progresses your narrative of Russia as the victim in the conflict it started – at the economic and human cost to its own people – to take Ukraine territory.

Thank you for an interesting discussion. This is why I have this throwaway: to talk about things beyond the soundbites in the media without worrying about the downvoters.

To play devil's advocate: why doesn't the US stop now? There used to be a Ukraine entirely under Russia's control politically. Now there is a West Ukraine that is entirely dependent on the USA politically, has Black Sea access, has the oldest city in Russian history, has the oil and gas pipelines running through it (and so provides a way to continue to pressure Russia economically), and has a largely pro-West population. What is to be gained (other than pride) by forcing majority Russian-speaking lands that got accidentally attached to an entity named "Ukraine" to be part of this brave new world?

And before you go "but borders", let me point out that the reason behind many wars in Africa were borders that were arbitrarily drawn by the colonizers for their own convenience, and that often split up historically homogeneous tribes, or forced mortal enemies to be "the same country" (Harari has the details).

Finally, about the "who is going to try to overthrow Putin" point. It seems ridiculous now, but this is exactly what the media were selling back in 2022.

This is like saying -- we just have to accept that England belongs to Italy because after all London was once known as Londinium and was one of the most important cities in the Roman Empire.

Hey, Turkey bit off a chunk of Cyprus as late as 1974, and they are US allies. The US itself has presided over redrawing the borders in Serbia in the 90s (and somehow in that case the justification of "an ethnic minority wants a chunk of land" was totally legit).

It was communism that fostered this independence movement of the eastern states, and it was the USSR that drew the arbitrary line soon after the revolution.

> What is to be gained (other than pride) by forcing majority Russian-speaking lands that got accidentally attached to an entity named "Ukraine" to be part of this brave new world?

If this really was Russia’s intent they wouldn’t have tried to take the entire country at the outset. And if this is some kind of liberation project for those long suffering Russian speaking minorities, I’m certain those being bombed aren’t welcome of it. There’s no noble intentions behind the inception of this war, but let’s say there was, those intentions seem to have since been contradicted by the human cost which Russia’s leadership has proven insensitive to

Minorities? Reality is a stubborn thing. The numbers: Russians are 71% of the population of Sevastopol, 58% in Crimea, 39% in Donbas (but in Donbas, 97% of people who identified as Russian spoke Russian, whereas only 41% of those who identified as Ukrainian could actually speak Ukrainian). These are 2001 numbers from https://en.m.wikipedia.org/wiki/Russians_in_Ukraine

And who, pray tell, is dropping bombs on these people? (and has been since 2014). Hint: it is not Russia. So they absolutely do welcome the protection and make up the majority of the fighting force currently advancing on West Ukraine. What is actually happening is in effect a civil war.

Edit: to the downvoters: which is it that you disagree with? That a chunk of a population larger than 50% is not a minority, or that people don't generally bomb themselves?

> Russians are 71% of the population of Sevastopol

Strawmanning again. That same census shows 17.3% of Ukraine identifies ethnically (or culturally) as Russian. But instead you want to split hairs.

> 58% in Crimea

Crimea is Russian in the pre-war border, and is irrelevant to this thread.

> whereas only 41% of those who identified as Ukrainian could actually speak Ukrainian

Kind of telling that non-Ukrainian speaking people are identifying as culturally as Ukrainian. It puts further doubt as to how much people inside the pre-war borders wanted to be 'liberated' by being usurped by Russia. Language != culture != nationality != support for annexation

All the same Sevastopol, which is the only majority Russian population in pre-war Ukraine that you mentioned, is not all of Ukraine. Very clearly Russia's play was for the whole country. The kind and noble angle you're presenting of Russia as liberator is either disingenuous, if you're trolling, or delusional, if you're being earnest.

> and make up the majority of the fighting force currently advancing on West Ukraine

Even if that's verifiable, there's no way of knowing how many are fighting by choice. Wouldn't be the first time Russians/USSR sent people to fight 'under pain of death'. And of course they aren't alone in this sort of conduct in war time.

> is dropping bombs on these people?

Both sides. Because of a war—I repeat once again—instigated by Russia. These populations wouldn't be caught in the crossfire of shifting battle fronts, if there was no... err.. battle.

So I'm done here. You aren't arguing in good faith, nor seem to yield to reason. Feel free to have the last reply.

Hey, I made you (and maybe a few other people) go look up those numbers to make sure this Russian troll isn't lying, and think about what they mean. That's already better than the usual "Putin evil, QED".

America has done a good job at nation building in the New Ukraine. They built a new country in Israel's image: ethnocentric and very militarized, with a strong warrior ethos. But you just can't resist adding a Gaza Strip, can you?

I think your timeline is off by about 2 decades. The nightmare period of Russia is not the current time, it's the 90's. That's when they were most wounded and the had the most economic turmoil. And just as you wouldn't have stopped Hitler by appeasing him after he grabbed the power, you won't stop Putin by appeasing him now.

If we are examining the equivalence between Putin and Hitler, and saying (aided by the passage of time so we can actually think calmly) - pressuring Germany was what allowed Hitler to come to power, is it not then true that this period where Russia was wounded and had all the turmoil is what allowed Putin to come to power?

Second question: who did the wounding? Who do you think the average Russian thinks did the wounding?

> is it not then true that this period where Russia was wounded and had all the turmoil is what allowed Putin to come to power?

Sure, that was my point.

> Second question: who did the wounding? Who do you think the average Russian thinks did the wounding?

It's... Hard for me to formulate a strong answer on this, but my impression is that Russia mostly did the wounding itself but the current average Russian probably blames either the reform attempts masking a power grab OR the west and the US for it's toils.

That's my point though: these leaders aren't aliens beamed down to Earth from space. They are the kind of leader a society elects as a sort of Hail Mary last ditch self preservation effort (yes, elects, in that they actually have support and are not usurpers).

As for the second part, let me retell an anecdote. I was once at a party (in the US) with someone who participated in "helping" one of the post-Soviet republics with reforming their industry after perestroika. After too many drinks he began to brag about how "these corrupt businessmen thought they were hot sh... for grabbing all that stuff, little did they know they were just handing it to us". There were a ton of vultures feasting on the USSR's corpse. Now, the fact that it came to that in the first place is absolutely the Soviet leadership's fault.

And it is also ultimately the current Russian leadership's fault that Victoria Nuland even got around to handing out those cookies 10 years ago.

US should return to isolationism now. It never was an actual superpower. It just convincingly played one from a distance. Nearly every US engagement in recent times just shown how inapt US is at effecting anything anywhere through military action. US getting directly involved in Ukraine will just clearly show vast scale of US military incompetence to China and anyone who could still have any doubts.

This is nonsense. The US advising Ukraine and supplying s limited amount of weapons has allowed them to hold out against Russia when they were supposed to collapse in a week. If anything, this war has shown Russia to be a paper tiger. They're literally resorting to WW2 era tanks at this point.

Keep in mind that Russia and the US are both nuclear powers, so that complicates things as neither Putin, Biden, or Zelensky want nukes being thrown around.

Between the US's actually functioning carriers, F-22s, modern tanks, and finally functional JSFs...I don't think Russia's untrained cannon fodder being supplied by civilian vans is going to win out.

That being said, the democratic countries in Eastern europe are tiny and most have a very small military presence. Without NATO, Russia could conceivably storm into those countries.

I don't think there is a good answer here. Either let Putin steamroll a chunk of Europe or spend a ton of additional taxpayer dollars. A little googling suggests the U.S. support for Ukraine is 1.5% of our federal budget, which is crazy high if you think about it.

Isolationism has its benefits and drawbacks of course.

> A little googling suggests the U.S. support for Ukraine is 1.5% of our federal budget, which is crazy high if you think about it.

Isn't it surprising how little this mountain of money achieves? It just slows down Russia at the unsustainable cost of Ukrainian lives.

Maybe US budget is so huge for other reasons than their military prowess? Maybe everything US does is just vastly overpriced for its value? Could American military be even more overpriced than American healtcare?

I'm just saying it's a ton of money. We didn't just donate a few billion and call it quits.

I think part of this is viewed as an ongoing expense where we're constantly giving someone weapons (Israel, Ukraine, whoever) in order to keep the Defense industry in business. It is a roundabout way to give our tax dollars to Raytheon and other firms without directly giving it to them.

Slowing down Russia at the cost of Ukrainian lives is a decision for them to make. You might feel differently if your country was being invaded. The US citizen should get a vote though if they're paying through taxes and inflation.

Overpriced? Almost certainly. Government isn't efficient. It's run much more efficiently than Russia or China though where much of the funding is siphoned off due to corruption. We don't appear to have that problem at least, although the Pentagon constantly failing audits is suspicious and something we do need to look into.

I could only find older expression of this sentiment towards Findland but I heard about it recently too, just didn't pinpoint the source and I can't find it now:

I thought it was obvious. Hey, someone downvoted me for it so they must have understood (that, or they reflexively downvote anything they don't understand).

If you aren't adding to the discussion (e.g., by being obtuse) that's reason enough for a downvote. And underneath it all you're quite brashly making a false equivalence.

You conflated WW1 and WW2 and yet give me lectures on style and judge whether the equivalence is false or not? There's a word for that. I don't think I am the one being brash here.

Now you’re strawmanning. Once I knew the argument you were making (which honestly wasn’t clear to me), the overall critique was correct and justifiable, but for one minor error (namely, Germany being in rubble after WW1). Just so you know, I didn’t downvote you.

The only miscalculation in WWI was that there wasn't allied parade in Berlin so Germans didn't understand how hard they lost. So reparations seemed like unfair backroom deal. This mistake wasn't repeated in WWII.

In case of today's Russia, Ukrainian parade in NATO equipment on the Red Square should teach Russians clearly how hard they lost so their ambitions are crushed.

You do realize that this is exactly why Russia keeps fighting? From the Russian perspective, the collective West has taken its nice mask off and will stop nothing short of what you are describing.

Yeah. And they are gonna fight to the bitter end. Nice mask goes off because Putin forcibly pulled it off. Remilitarized Europe won't get calmly mothballed. There will be a NATO parade on Red Square. If not in 3 years then in 20 when soldiers that Europe trains now reach middle age, positions of influence and feel like their lives weren't good because they were robbed of an easy win against Russia.

Putin started this because he thought Europe got defanged and is no longer a monster it used to be. But its demons were only asleep and Putin just woke up all of them.

The most surprising thing to me about this is just how... common these market moves are. Seeing so many big swings, even in the early days of the country, really drives home the idea that actually, things aren't as bad as they always seem when you're going through them.

My takeaway was the exact opposite: in the 1930s, things really were as bad as they seemed, and the U.S. was justified in taking extreme measures to avoid it happening again.

4. Spending the tax money like crazy, to give the poor some money to buy things.

Hoover Dam, Golden Gate Bridge etc are nice takeaway of that generosity frenzy. Too bad during COVID gov just gave cash, not getting any infrastructure in return.

COVID wasn't a lack of employment problem, everyone had jobs, the government decided to pay people to stay home. It was a handout specifically aimed at not building anything at all.

The government persisted with the failed policies, lengthening and deepening the Depression. Central economic planning simply never is able to do better than free market forces.

That's not really true. Just because central planning be done stupidly doesn't mean it never works. Check out the number of countries that don't have something like a central bank stabilizing their currency which is approx zero out of 200 or so countries.

> business cycles are natural and periodic like a pendulum swing.

But how long the downturns last is a policy choice:

> I would summarize the Keynesian view in terms of four points:

> 1. Economies sometimes produce much less than they could, and employ many fewer workers than they should, because there just isn’t enough spending. Such episodes can happen for a variety of reasons; the question is how to respond.

> 2. There are normally forces that tend to push the economy back toward full employment. But they work slowly; a hands-off policy toward depressed economies means accepting a long, unnecessary period of pain.

> 3. It is often possible to drastically shorten this period of pain and greatly reduce the human and financial losses by “printing money”, using the central bank’s power of currency creation to push interest rates down.

> 4. Sometimes, however, monetary policy loses its effectiveness, especially when rates are close to zero. In that case temporary deficit spending can provide a useful boost. And conversely, fiscal austerity in a depressed economy imposes large economic losses.

> But how long the downturns last is a policy choice

Maybe I'm projecting, but you say this like it's just a fact and that there are no tradeoffs. Keynes was a smart guy, but his word isn't gospel. It's not as simple as printing money to reduce interest rates and then magically depressions end. Printing money and lowering rates can easily lead to inflation (which would make everyone even worse off than they already are) if other underlying issues aren't addressed. We're literally seeing that in real time with economic policies form 2020-today.

So yea policy can influence how long they last, but that goes for both directions (shortening or lengthening/making worse). Striking the right balance to like "optimally" shorten/ease a depression is incredibly hard, and (shocker) tends sows the seeds of future economic downturns.

There is very likely no policy that eliminates the cyclic nature of markets/economies; it's inherent to (essentially required for) how they function.

>inflation (which would make everyone even worse off than they already are)

Is this true though? Doesn't inflation just redistribute wealth rather than destroy it? We measure inflation through change in prices which are just a measure of supply and demand (dis)equilibrium, I thought.

Inflation concentrates wealth in those with the power to inflate. This is usually strictly worse for the economy because the power to inflate is rarely vested in people capable of effectively deploying that captured wealth as capital. If this destruction of capital exceeds the rate of capital formation then the necessary decline in investment will reliably erode the economy for everyone, except perhaps for those proximal to those with the power to inflate (see also: the Cantillon effect).

The cantillon effect is mostly a meme. If it was such a powerful explanatory device then how come nobody is talking about the inverse cantillon effect which is much stronger and caused the great depression? You know, the idea that price falls propagate through the economy. It would appear to be much more dangerous, since it can be conducted by anyone who is holding onto money and every successful attempt spurs on more imitators. Since the imitators are betting on the productivity of doing absolutely nothing, capital formation will cease until there is a shortage of capital and ... surprise, a forward cantillon effect occurs through "unhoarding". We somehow end up with a business cycle theory that actually makes sense compared to the Austrian economist one. A lot of them seem to think that the business cycle is some nefarious plot by central banks instead of a disruption in economic communication induced by market participants following their own interests.

Inflation benefits debtors, and hurts creditors. But if inflation is controlled and predictable, those contracts will price that in or renegotiate. On the long term, inflation has no real impact on the economy.

Uncontrolled, unpredictable inflation (40%)(Zimbabwe, Turkey) is the problem as it incurs more costs on updating prices and renegotiating contracts, which introduces severe distortions on the economy. But we're not anywhere near that.

Keynesian economics can certainly work to help end something like a recession or depression (and we can see that when FDR tried to pull back on those ideas unemployment jumped back up again).

My beef with it is that it doesn't seem to be a sustainable system in the long term just like the previous system also had issues. We didn't have a great depression in 2008 (a very nasty recession instead), but the quantitative easing then and during Covid is driving inflation wild. The official numbers are generally fine, but they don't include all sorts of items that have gone up an incredible amount and are thus misleading. I'm sure some of it is corporate greed or standard supply/demand (e.g. a wood manufacturing plant going offline making construction material costs soar), but a lot seems to be because of the insanely high printing of money that has to be carried out in order to inflate away the massive runaway national debt.

So the Keynesian toolbox that can be used to get us out of something like a depression also is ultimately our downfall in the long run as our leaders can't or won't use it responsibly.

There's a blip now because of the pandemic policies - hand people a bunch of cash to sit at home which means less goods made, let them out again where they can spend it - prices go up. I'm not sure that's Keynes fault - he never had a covid policy.

Truly great concept except this "sometimes" of point (1) gets sacrificed to political expediency, and Keynesian stimulus ends up being the normal and expected rather than an emergency measure.

It's hard to resist and not to always print money, not just occasionally, and not to (just about) always run a large deficit, not just occasionally, and not fund petty hobbies - not just productive infrastructure - with borrowing.

> It's hard to resist and not to always print money, not just occasionally, and not to (just about) always run a large deficit, not just occasionally, and not fund petty hobbies - not just productive infrastructure - with borrowing.

At that point it stops being Keynes (stimulus) spending and just becomes spending.

The point of Keynes, especially in light of when he originally wrote (the 1930s), is to boost demand to help an economy get back on its feet. Once it's running fine then the "extra" spending can be dialled back.

Of course there could be other reasons why government wants to continue (deficit) spending, but those are separate from Keynesian stimulus.

downturns are more due to the different timescale between investments and business cycles / market saturation. Current Market returns are due to previous allocated capital, investor chase past results hoping the trends continues, but market saturation or other shocks happens, scaring investor who rush to liquidate their positions, cratering the prices. Companies to keep certain profitability levels in the short term cut costs to the extreme, slowing growth/expansion and laying off workforce. IMHO to contain bubbles and busts, a lot more business/market data should be aviable to make informed investment decisions and make long term investment fiscally advantageous compared to shorter holdings

There's another name [0] for the "business cycle" and it doesn't rely on superstition either. Unfortunate that theory predicts those crises will trend getting worse and worse until the eventual breakdown of the system.

Its why the rich always get richer too. They have the capital to buy into inevitable downturns and ride the bull run into orders of magnitude increases of wealth. Everyone else just loses their job and has to pay for rent and food out of savings and loses their generational wealth in the process.

I think rich get richer because of a bunch of reasons but not really because of “buying when there is blood on the streets” or “timing the market” if you prefer.

Reasons include:

* Children inherit wealth and knowledge of how to build wealth

* The children are doing this rather than trying to leetcode to get their first job (or rack up debt to get qualified for it etc.)

* Connections

* Compounding (despite corrections)

* Political influcence

* Can afford to hire tax/law people to avoid tax

* Tax law favours the rich. You pay no tax on a billion in capital gains if you never sell and if that yields you 50m you pay tax on that but let’s say it is half so 25m that is 2.5% of the wealth but if it goes up 75m over the same period that is tax free so you paid 20% tax on the increase in net worth. Compare that to a worker. And this is without doing any tax avoidance!

* To avoid tax at all in the previous example get the corp to buy back shares instead of paying dividends then live off borrowed money.

> * Children inherit wealth and knowledge of how to build wealth

that knowledge is so important. When i was a kid all I was told over and over was "get a good job in an office so you don't have to work like i do". This was coming from blue collar oil and ranch hands in West Texas so that's what i did and it's worked out pretty well for me. However, I'm teaching my kids how to build wealth and that a well-paying job is an income stream to assist with that but not the whole answer.

periodic yes, predictable, maybe? Like I can say with absolute certainty that there will be yet another period of growth and yet another recession. All of this has happened before and all of this will happen again.

I've always heard that deflation is awful and must be avoided. Following WWI, this marks a period of "13 Year Deflation" from ~1918 - 1931, but this includes a period marked "prosperity" from 1922-1929, though commodity prices then dive as the depression deepens. But what conditions made deflation and growth possible together in the 1920s?

Fed chair bernanke famously said "the us government has a technology called a printing press" to explain why deflation was in no way to be feared, bc unlike inflation it can be fought easily and without serious drawbacks.

Deflation is good, it means cheaper prices. A deflationary spiral due to insufficient money supply despite robust economic fundamentals can be really bad in theory sure, but it can't happen unless the monetary authorities are totally negligent and incompetent, as happened in the great depression. All you have to do is print more money and problem solved. We don't expect it to happen again because we learned from it.

As someone who has lots of debt, I would prefer slow, but subtle inflation.

I look forward to minimum wage jobs being 25 dollars an hour, and still poverty wages - because then the debts I have will be roughly half what they are now in constant dollars.

Based on prior experience? No, I dont think so - interest rates go up, and they go down. I look at all the folks who bought houses in the early 80's between appreciation and inflation they won in the end.

This also works out for unsecured debt too largely.

Everything else being equal, you almost always win when buying a house in inflationary times. Even if you pay a high initial rate you can always refinance to a lower one later. If rates stay higher for longer than anticipated your income is most likely rising as well. In either scenario your debt service expense is trending down as a percentage of your nominal income, and your asset is trending up with inflation.

But surely you notice that when interest rates go up and down, that movement is tied to changes in expectations of inflation?

The '80s homebuyer did great on their purchase, but not because borrowing at 20% was such a steal. They profited because their home subsequently went up in price faster than inflation did.

The ultra-wealthy can borrow phenomenal amounts of money at low interest rates, which has two effects. First, as you said, is that during times of great inflation they come out ahead (also because they manipulate the broader economy to inflate). Second, is that borrowing doesn't count as earned income and therefore is not subject to income taxes.

I think we should outlaw billionaires. The idea that a sole individual could hold so much economic, societal, and political power is totally fucking insane.

I've heard that the ultra-rich borrow a lot against potentially illiquid assets to avoid realizing gains and taxes, but I'm confused how it works long term. Do you just keep taking out new debt to pay back your old debt, and continue doing that until you die? It seems like eventually you would need to sell something to pay back your older creditors.

I guess if you have, say, $50 billion in assets, you can take out a new $5 million loan each and every year, and by the time you die, and never have to pay yourself back. You've barely leveraged 1% of your assets. Their reality is unfathomable to us little people.

$5 million, to someone that rich, is like $50 dollars to us. It's chump change you might find laying around your house.

Furthermore borrowed money increases the money supply, and at that scale, the money you're borrowing can even be used to increase the price of the assets that you're using as collateral, allowing you to borrow even more.

It can also unwind just as quickly if you need to pay those debts back in a hurry, causing your asset prices to tumble on the way down. But if you're big and have borrowed enough money, whole jobs and industries will be dependent on your continued solvency, and so you can sometimes maneuver to put the public on the hook.

In the context of the original chart which covers a long period of US history ... is Bernanke's statement still true for most of it?

Clearly, I am not a monetary policy buff, but certainly I've heard people talk about the US getting off of the gold standard in 1971. When the currency is by policy backed by something, you can't just print money (unless you dig a new mine, I suppose), right? When I google around for what our policy was in the 1920s, I see that it was a bit complicated in that many countries suspended the gold standard during WWI and in some cases there were pegged exchange rates, and the US intervened in gold imports.

The standard of living in Japan for the vast majority of people is orders of magnitude better than it is here. It might not look good according to metrics that optimize ploughing society's wealth into the hands of a few billionaires, but it says something that an Uber delivery person can live walking distance to the popular restaurants that he delivers from.

Lots of things about the Japanese standard of living have little to nothing to do with monetary policy. Being able to park your bike just about anywhere without locking it up and without worrying about it being stolen, for example.

>have little to nothing to do with monetary policy.

False. A monetary policy that prioritizes universal access to basic needs leads to less overall crime. It may not be sufficient, but it is a major factor[1].

> The standard of living in Japan for the vast majority of people is orders of magnitude better than it is here.

But is that because of their economic policy or because of social norms?

> It might not look good according to metrics that optimize ploughing society's wealth into the hands of a few billionaires […]

Sweden also has a pretty good standard of living, less inequality than the US, decent economic growth (better than JP, lower than US), and has more billionaires on a per capita basis than the US:

People choose to vote for / elect people who are willing to implement various policies to achieve it. What is acceptable to the population is (partly?) determined by the norms of that population and society, and the acceptance of various ideas will determine what politicians will campaign for.

Japan's economic system was crafted in post-war reconstruction by General MacArthur. It's literally the furthest you can get from "social norms precede policy."

I think you're both right. IMO, Japan has a very high standard of living, but they could also be better off today if they'd been looser with fiscal spending (and spent that fresh-printed money wisely). For example, one of their major issues is an aging population; they could have directed spending towards subsidizing childcare, fertility treatment, parental leave subsidies, or even offering a salary to stay-at-home parents, to compensate and incentivize that valuable work. (They do have some of these policies, but their low inflation suggests they had room to do much more!)

Every nominal asset that can be sold to take advantage of lower prices on goods and services is someone else's nominal liability that they have to cover with weakened earning power. Deflation is straight up bad compared to mild and predictable inflation, it's easy to fight off sure but it's definitely something to avoid.

> […] but it can't happen unless the monetary authorities are totally negligent and incompetent, as happened in the great depression.

Or if you do not have monetary policy flexibility, like when you're on the Gold Standard, as happened in the Great Depression (until FDR went off of it).

See Bernanke and James (1990):

> However, Temin (1989) argues that, once these destabiliz- ing policy measures had been taken, little could be done to avert deflation and depression, given the commitment of central banks to maintenance of the gold standard. Once the deflationary process had begun, central banks engaged in competitive deflation and a scramble for gold, hoping by raising cover ratios to protect their currencies against speculative attack. Attempts by any individ- ual central bank to reflate were met by immediate gold outflows, which forced the central bank to raise its discount rate and deflate once again. According to Temin, even the United States, with its large gold reserves, faced this con- straint. Thus Temin disagrees with the suggestion of Friedman and Schwartz (1963) that the Federal Reserve's failure to protect the U.S. money supply was due to misunderstanding of the problem or a lack of leadership; instead, he claims, given the commitment to the gold standard (and, presumably, the ab- sence of effective central bank cooperation), the Fed had little choice but to let the banks fail and the money supply fall.

> This book offers a reassessment of the international monetary problems that led to the global economic crisis of the 1930s. It explores the connections between the gold standard--the framework regulating international monetary affairs until 1931--and the Great Depression that broke out in 1929. Eichengreen shows how economic policies, in conjunction with the imbalances created by World War I, gave rise to the global crisis of the 1930s. He demonstrates that the gold standard fundamentally constrained the economic policies that were pursued and that it was largely responsible for creating the unstable economic environment on which those policies acted. The book also provides a valuable perspective on the economic policies of the post-World War II period and their consequences.

Following the rules of the gold standard is what caused the initial "negligent and incompetent" action. Of course later (1937) on they raised rates too soon (and the government dialled back deficit spending), which caused an economic slowdown.

It was not until the giant stimulus packaged often referred to as "World War Two" that the economy picked up again.

> I've always heard that deflation is awful and must be avoided.

That doesn't mean anything. People talk about god/gods all the time, it doesn't mean they are real or exist.

Inflation/Deflation are meaningless without linking them to the system in question. Growth also, in my opinion, has little to do with inflation/deflation and more about the positive inflow of energy into the economy.

I think deflation independent of anything else is neither good or bad. Deflation gets a bad rap because it tends to correlate with market crashes and contractionary periods. If you are a senior on fixed income, or have a ton of cash, it is better than high inflation.

This is an odd statement to make, in most contexts deflation is good for the economy. It is mostly when deflation is coupled with an asset bubble and large underlying debt that it's an issue and leads to a financial crisis. Why do you think deflation is bad?

When your money becomes more valuable if you don't spend it, people spend less, which depressed prices further, so people spend even less, which even further depresses prices.

This mixes up the reason and the cause. A deflationary spiral occurs when you have a financial crisis, e.g. due to a debt-based asset bubble, and the economy is not strong enough to stimulate growth through policy changes, e.g. interest rates are already zero etc. This then in turn leads to reduced spending to ensure liquidity, that is reduced demand, which leads to lower prices, which is deflation. Deflation is the result, not the cause. From that point onward, yes, it is possible for the situation to spiral in a feedback loop, but deflation is not why the spiral started.

Yes, but this is easy to avoid. It's only happened when the governmental authorities foolishly believed they should respond to deflation with austerity, which is now obvious to us that this is backwards. See https://en.m.wikipedia.org/wiki/Bernanke_doctrine

That said, the fact that austerity has been tried recently suggests the perverse impulse to respond to deflation with belt tightening instead of expanding credit is still with us. But all we have to do is just print money to match the deflation. The 1990s through 2019 are a great example, there was constant economic deflation because of new technology and the fed just printed credit like crazy to match said deflation and keep the inflation at 2pct.

The pie was getting bigger, so eroding the value of each slice to make it a smaller portion of the pie kept slice sizes stable while not making anyone lose pie.

They had an easy time with that. Now that the pandemic caused real eocnomic inflation due to supply shocks, dealing with excess inflation is a lot harder. The only way to keep pie slice size stable is to take away pie from someone and nobody wants be the loser, so capital and labor are in a game of chicken to see who blinks first and has to eat more of the inflation.

> the fed just printed credit like crazy to match said deflation and keep the inflation at 2pct

There's no rational basis for the 2pct inflation target [1], it's entirely baseless, in some sense it's now a matter of conservatism, mere tradition from a random fad decision in the 90s.

And the point is that monetary expansion directs the energy of the economy and effectively steals savings, forcing the economic energy of people into consumerism and CEOs pockets.

> There's no rational basis for the 2pct inflation target [1] […]

Except that it seems to work.

Hitting an inflation rate of exactly 0% is practically impossible: you're going to be either a little high, or a little low. So the option is: do you want "too high" or "too low" (negative)?

In the last little while how we've all seen how painful high(er) inflation is for people. Lessons from periods of the 1930s (and others in the linked-to PDF) show how bad deflation is.

A "little" high seems to have been a pretty good compromise.

This is not true though? Japan had interest rates around zero for decades and likewise inflation which bounced around the zero mark, sometimes over, sometimes under. It is both possible and feasible, it's simply a matter of policy. See [0] and [1], choose "max" as the date range to see what I mean.

> Under Kuroda, the BOJ deployed a huge asset-buying programme in 2013, originally aimed at firing up inflation to a 2% target within roughly two years.

> The central bank introduced negative rates and YCC in 2016 as tepid inflation forced it to tweak its stimulus programme to a more sustainable one.

Yes and Japan's economy has been stuck in the 90s for the past 30 years with very little growth.

What you're describing wasn't their goal, they have been keeping interest rates at ~0% since the late 90s to avoid deflation and to stimulate the economy (and therefore increase inflation) with limited success.

The 1930s show the consequences of inflation, speculation and credit expansion, and then bungled government response that dragged out economic contraction which is needed to clear out malinvestment.

Any common person realizes their ability to lead a dignified life is being squeezed out by monetary expansion gone amok, with those closest to the govt spigot getting the benefits and none of the costs (cantillon effect).

And it brings up a good point which no one answers satisfyingly: why shouldn't the average person just enjoy price savings produced by technology?

> The 1930s show the consequences of inflation, speculation and credit expansion […]

The 1930s were nothing special when it comes to wild swings in prices (as the article show), speculation was not new (see canal mania, railroad mania, etc)

What is special is the post-WW2 era (where there was no deflationary bust, especially after a major war), and the decades that followed (when there was no gold standard to handcuff monetary policy, and when Keynesian economics allowed for fiscal flexibility).

> And it brings up a good point which no one answers satisfyingly: why shouldn't the average person just enjoy price savings produced by technology?

There's a difference between deflation through innovation, and deflation through economic turmoil (e.g., mass unemployment, collapse of aggregate demand).

One of my favourite examples of 'invisible deflation' that no one notices (often while they're complaining about inflation) is a 1991 Radio Shack ad:

> that getting overly excited about things seems to just be a thing humans tend to do

human nature is to avoid discipline when they're comfortable and set the stage for a bubble & contraction, exactly what happens with artificially low interest rates and speculations like the manias you brought up

I'd still like to know according to who. Practically everyone agrees the economy is worsening for average people during many decades of nearly universal control by "mainstream" economists, advisors and bureaucrats.

> Practically everyone agrees the economy is worsening for average people during many decades of nearly universal control by "mainstream" economists, advisors and bureaucrats.

Look at the chart that this story is about: when things go negative, what do you think happened to people's employment opportunities? What do you think happened to their debts (deflation makes it worse)?

Do you want to perhaps look at the economic historical record of the ~80 years before 1945:

the dominance of equities is something precisely caused by the shift in the monetary system in the 1970s, which ushered in devaluation of money and forced ordinary people to seek yields from investments in businesses

While deflation sounds good, its is definitely bad. When prices are falling, this provides an incentive to firms and consumers to delay purchases since prices are expected to be cheaper in the future. This reduces aggregate demand, which means goods get cheaper due to less demand, causing firms to have to fire people due to lower, causing greater economic decline that spirals out of control. We now know that deflation was a primary cause of the Great Depression.

Neither one of those is true. So long as it is not extreme, a decline in the price of goods means consumers have greater purchasing power, more financial security and hence more flexibility in their spending and saving. All of these are good for the economy as an aggregate.

Except your debts start increasing even while you're continuously paying them off and investment becomes much more lucrative.

Deflation benefits those who have a lot of capital and can invest it into ~ zero risk instruments like government bonds the most (e.g. that's basically how the rentier/aristocratic class in the 19th Britain were able to maintain their lifestyle without doing anything productive, government bonds were yielding 4-5% while the value of their capital was going up due to near continues deflation throughout much of the century).

On the other hand if you're a heavily mortgaged farmer you were basically screwed if the price food went down (that's why free-silver/loose monetary policy was so popular amongst farmers back in the 1800s in the Midwest and in much of US).

Let's say the price of everything goes down. And let's say you owe money when it does. Now everything is cheaper (including your labor, because the price of everything went down), but you still owe the same number of dollars. That hurts.

And if you say "wages won't go down", then you're expecting that everything else goes down (including the price of whatever your employer makes), but your wages magically won't? It would be nice... but don't hold your breath.

but that would only happen under monetary contraction, and the norm now is monetary expansion which siphons off money from savers and redirects it into the pockets of asset holders and "Cantillionaires", and this also means you get paid less with a static wage unless you get raises which for many people is hard unless they're constantly job searching which sucks anyway

This logic doesn't work. The past few decades have seen steady to strong inflation, while purchasing power after adjusting for inflation, depending on the country, has either not kept up with it or has straight up gone downwards. So in other words, the price of everything has gone up, but not wages. So I don't really see how the price of everything going down would mean wages going down either.

When prices rise, we'd expect revenues to rise, which is not necessarily given back to workers in the form of buying power. (See grocery stores having record profits as prices have rised, for instance - that increase in profits is probably in part the gap between prices and wages showing up.)

However, no company is going to do that the other way around - if their revenues fall, they will either cut wages or fire people in order to still be profitable, so deflation should show up faster in loss of buying power too. Companies don't generally just accept lower profits, and shareholders especially do not accept this.

> So long as it is not extreme, a decline in the price of goods means consumers have greater purchasing power, more financial security and

Deflation means that people's debt becomes more of a burden. I'd hazard to guess that poor people have more debt that rich, and so deflation would be worse for the poor.

but debt actually having a bite cuts both ways and bad businesses should be on the hook for their debts, and middle class people who carefully save over their entire life deserve to not have their savings inflated away or otherwise forced to invest in businesses to preserve or grow the purchasing power of savings

Regardless of what one thinks about deflation in general, deflation TODAY in the United States would be extremely bad(due to the debt load). That said, you should obviously want the "cost per unit of X" to be deflating. dollars per teraflop should always be falling. dollars per kilowatt hour should always be falling.

Except we really need deflation. A dollar today is 2.6x less than a pre-2021 dollar. People can't afford homes anymore, and it's not entirely because of the interest rate, but because everyone's home has doubled in price since 2020.

The market is locked up. How many families are making 133k+ a year to make the 3x rule for a 400k tiny townhome? The US Census reports the average household income is 75k.

The Feds and Deep State have played with people's lives for too long, pretending like they can offer security and order. In reality, they've screwed over the middle class.

People have a strong and well-founded attachment to nominal values in the economy. You pay your rent or mortgage with a fixed quantity of dollars, so as a salaried employee certain pay cuts are intolerable, so employers balance their falling nominal revenues with layoffs instead of pay cuts.

These nominal agreements are significantly less flexible than real-valued ones; people are much more able to buy fewer steak dinners when they're $20 instead of $15, and much less able to stay in their house when their paycheck is $1500 instead of $2000.

Economics 101, deflation is very bad. Basically it is because it directly leads to economic contraction. Why produce something if you're not sure you're going to make the necessary money if you sell it, or wait if you can buy it for cheaper.

This is fundamentally flawed, I'll rather refer you to a thorough article on the subject [0]:

> Most of the time, deflation is unambiguously a positive trend for the economy, but it can also under certain conditions occur along with a contraction in the economy.

The heading even leads with "why is deflation bad for the economy".

Obviously there are situations where it is good and for certain people, say a right sizing of an overheating economy/sector but on the whole, and more generally, it is bad, not something you look to as fine or alright.

It would be helpful if you could actually read the article. Then you'd see that the article outlines some specific situations where deflation is bad for the economy, but concludes that it is good in general. You'd even take away as much if you only read the key takeaways section, but sadly that seems to be a tall order.

There is plenty of empirical evidence from the ~130 years or so prior to the Great Depression which shows why deflation (or rather restrictive monetary policy) was bad, stifled economic growth and lead to permanent boom and bust cycles and generally very high price volatility.

I've read it before my prior response and it ends off with:

"A little bit of deflation is a product of, and good for, economic growth. But, in the case of an economy-wide, central bank-fueled debt bubble followed by debt deflation when the bubble bursts, rapidly falling prices can go hand-in-hand with a financial crisis and recession."

Saying an economy-wide, central bank-fueled debt bubble followed by debt deflation is bad is very different to saying that deflation is very bad in general. This is simply trying to reframe your argument after the fact. Deflation isn't the cause of economic contraption as you said, it is the result.

I'm pointing out the article you referenced is saying its bad, the reason it says is exactly what I'm saying. It's fine short term but it's bad overall.

They're just saying in our debt fueled world, you can't merely print money to get out of jail free in a deflationary scenario as eventually the debt obligation gets too large relative to your shrinking economy size.

We live in this world unfortunately where it's bad, in a hypothetical world without all the debt, it's still bad in the long term for the other reasons I've mentioned.

Deflation is just prices going down. There is a difference between the good years with prices going down but people have loads of money to spend and the bad ones of prices going down because everyone's broke.

>I've always heard that deflation is awful and must be avoided.

Because most modern economists are state-funded and the state benefits handsomely from the ability to print money. If you look back before economics got institutionalised you'll see a consensus that inflation is far worse than depression; plenty of states have been destroyed by debasement of the money supply (as far back as the Roman Empire artificially devaluing its currency leading up to its collapse), but there hasn't been a single one destroyed by the value of its people's money increasing.

Because deflation can only be transitionary; people need food and housing and other necessities, so there's a limit to how much they can reduce spending, and once that limit is reached the economy has just shifted to a new equilibrium, one with less spending and more savings than before. Inflation on the other hand (when it's caused by printing money/defacing the currency) has the power to destroy 100% of the populace's wealth, as we saw in Weimar Germany and Zimbabwe.

Just because an economist puts a name on an economic trend like "secondary post war depression" doesn't mean they understand it. The economy goes up, it goes down, it goes up, it goes down, it goes up, it goes down, economists usually don't know why or how.

I like reading stock news twice a day. Once, during trading when they have no idea what is happening in the trenches. And then again in the evening, to see what creative narrative msnbc came up with to justify a total about-face from what they wrote a few hours earlier.

I regularly see some article on the iPhone stock app saying something like "Dow (rise|plunge) on <reason>, markets wrapped", five minutes after open. Look guys, "markets wrapped" means "it's after close" and that doesn't happen for another 6:55 hours...

Not to mention -1% is not a "plunge", it is well within the normal variance.

Wat? Macroeconomic observations don't individually track every single microeconomic occurrence and assign a root cause that "Bob did it". There are many possible factors leading to recession but no singular root cause because it's macroeconomic, some include:

- OXPC: Over-expansion of productive capacity

- Contraction of credit

- Contraction of demand

- Knock-on effects of layoffs harming other sectors

Could somebody ELI5 for me why, during periods of both prosperity decline, the economy movement is stable for the most part, but in order to cross over from decline->prosperity or prosperity->decline, there is a huge and sudden swing?

1837 and 1873 appear to be bubbles bursting (maybe) - is every sudden downswing a literal, practical panic?

And why are the upswings just as sharp? What is happening practically during those moments that make the swings so sudden compared to economic activity "during" a prosperous or downturn period?

There's a momentum to consumer confidence and credit crunches. Folks were talking about the 2008 crash for about 18 months before it happened. We're staring down something on the horizon now, and I'm sure someone more economically minded than me can envision what it is, but will it hit in 1 year, 3, 5?

Everything is usually sunshine and roses until it's not, and then things stay conservative until there's some sort of all clear.

People are moody, and will ignore the problems and keep pushing further investment / work harder / we need to hire now! or nobody can make money / why bother going to work / fire people or get bankrupt! for way longer than it makes sense.

It's alright, 'cause the historical pattern has shown how the economical cycle tends to revolve in a round of decades. Three stages stand out in a loop. A slump and war, then peel back to square one and back for more. Bigger slump and bigger wars, and a smaller recovery. Huger slump and greater wars, and a shallower recovery. You see the recovery always comes 'round again. There's nothing to worry for, things look after themselves. There's nothing to worry, if things can only get better.

There's only millions that lose their jobs and homes, and sometimes their accents.

There's only millions that die in their bloody wars, it's alright.

It's only their lives and the lives of their next of kin that they are losing.

Don't worry, be happy, things will get better naturally.

Don't worry, shut up, sit down, go with it and be happy.

cycles are natural. instead of fighting it and treating the system as a fragile too big to fail egg, maybe we embrace the pendulum and think more about antifragility? Taleb's antifragility concept, if it's an obscure matter.