What’s the state of freelance and entrepreneurship in countries where there is a socialized healthcare system? I think this would be easy to look up for places like Canada, UK, France etc?

Looked it up for Canada. 54% of all private employers are companies of 1-4 people.

"Of the 1,167,978 employer businesses active in Canada, micro-enterprises (firms with 1 to 4 employees) constitute 54.1 percent of all private employers, which is the largest SME group."

You're not wrong about the stat, but I'd also point out that we have a political system that isn't as easily manipulated by big companies, meaning there's less power/incentive to be a big company (such as there is in the US).

Canadians seem to distrust big companies more than Americans do.

I would point out the fragmentation of workers is multivariate far beyond just the single payer + single provider healthcare system .

I don't think it's as complicated as all that. I am in Canada and the truth is with 35 million people, you just aren't going to have giant companies with 10,000+ staff. Outside of a few companies in oil+gas, forestry, transport, telecom and banks, most companies can get by with a few hundred employees.

Of course, some of Canada's globally renowned companies have faded too. Blackberry used to employ 14,000 people in Canada as recently as 2011, but they're probably about 20% of that size today.

Even though we have universal health care it is not free and not paid from taxes but from individual direct fees. the minimum monthly rate is currently a whopping ~400€ (450$). They will decrease the minimum rate to 200€ next year.

As far as I understand the German system has lots of limitations on freelancing though, to protect the employees. For example, as a developer you can't freelance for one client only, as the client company could be in hook for employer payments. You need at least two customers.

Not a German national, so I'm happy to be corrected.

No, you're basically right. But it's more like a grey area: There are ways to circumvent this. But of course this introduces a lot of unfairness because rookies usually will be out of the know.

Kind of reminiscent of a lot of tax-scandals that come along regularly: Usually nothing illegal but because of well meant intentions created a complicated system, gaming the system benefits only those that are able to do so.

My understanding is that the German health care system still has disincentives for sporadic work, because you pay a higher rate under the philosophy that "you have to insure yourself first, and make up for the expected lulls in income" or something like that. I read stories on reddit about immigrants getting burned by that when they were self employed.

The biggest disincentive is the progressive tax-rate.

But you stay on your public health-care plan as long as you don't reach a threshold of time spent per week. But of course, if you're an immigrant and never were covered by public healthcare then yes, you'll get burned.

Interestingly, those nations also have other regulations which protect labor, but may also make it slower and more difficult to hire/fire rapidly. So there's a range of factors beyond just universal healthcare at play.

I suppose we should also balance out how work is structured around those countries. Some governments prefer setting up and staffing their own agency for a given sector or situation rather than going full outsourcing. So people who would be working in the private sector still end up in public jobs even with a socialized healthcare system.

Usually in Europe/Japan/Australia/Canada there are fewer entrepreneurs. Maybe its because a wider safety net and narrower differences between rich and poor makes the leap to start a business less rewarding and worthwhile. Maybe people are less comfortable with taking risks.

Sweden is second only to Silicon Valley when it comes to unicorns. My friends there actually credit their safety net - it’s easier to take risks when you know if you fail you won’t end up sleeping in the street.

Founder from Europe here. When I made my decision to go self-employed most people and relatives thought I was foolish. The more so, the lower your/their social class or status is.

I too relate this mindset to our safety net.

But: The upside of being employed is very little risk of anything and a lot of paperwork/bureaucracy is done for you (Healthcare, unemployment insurance, retirement, accidents, your taxes etc). You'll pay a hefty premium for being employed but then again most others do too. So going self-employed is not just a bad deal in terms of risk it is also bad in terms of non-income related extra-work you have to take on.

I'm not talking about countries that have a more socialized, or social democratic, or even outright socialist system. I'm imagining the U.S. in its free enterprise self-made glory with stronger social safety nets, at least for the net most pressingly attached to employment status.

Social democracies are pretty much capitalist economies with better social safety nets and somewhat higher taxes than the US -- and you can't get a better safety net without increasing taxes to pay for it.

Despite the word "socialism", most socialist and social-democratic political parties in Europe are not trying to replace the market economy with socialized ownership of the means of production.

Free enterprise coupled with a decent safety net is exactly what those countries you Americans deem Socialist are like. On top, they rank higher than the US in terms of economic freedoms, while some got more self made billionaires per capita than the US.

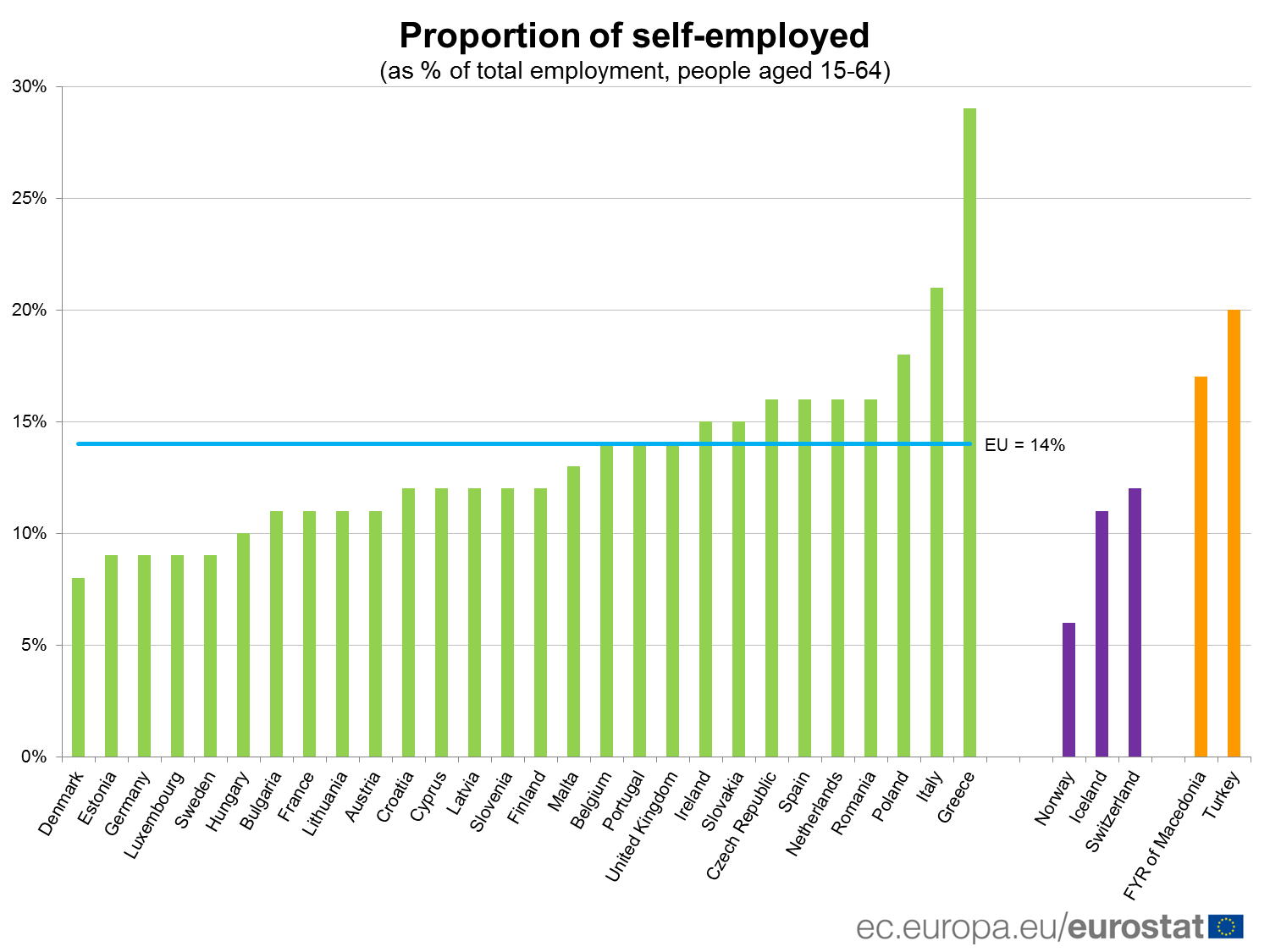

Freelancing? It varies greatly country by country. Easy and cheap in the UK, Ireland, New Zealand, Australia. Difficult and expensive in Germany. Moderate in Sweden and Canada.

Universal healthcare would actually make it much more affordable for employers to hire people too. So they could hire more people and maybe even pay them more.

There's not actually /insurance/ except for in the largest sense; it's more about health cost payment, cost control, and how badly individuals can be excluded or directly charged if coverage isn't required for all at the same input rate.

I am all for requiring everyone to be part of the same single coverage pool so that the costs of medical coverage in society are more fairly distributed across all. In that respect I also support /broad/ and /generic/ taxes on things that are known to be unhealthy; such as specific addictive recreational drugs. (For example, don't tax only soda, but it's OK to tax all drinks that aren't water.)

How are you so sure of this? I don't think we have conclusive evidence of this. It depends on a bunch of factors, among them is what government revenue would fund it.

Absolutely. I'm planning to move into full-time freelancing work next year, and health care is the most unsettling part of this move. It's the most unpredictable aspect of moving into a full-time freelancing role.

1. Coverage is more expensive for lesser benefits.

2. Year-over-year changes to costs and benefits are less predictable.

2b. Continuity of coverage may itself be at risk with pre-existing conditions returning to the political debate.

If you have basic, predictable medical costs — and believe that you will stay in that bucket — these concerns may not be very relevant to you.

But a lot of people don’t fall in that bucket or aren’t confident that they’ll stay there. For these people, this adds a big risk to venturing out as an entrepreneur or freelancer.

A wholly privatized, largely deregulated health care market is toxic to entrepreneurialism because of these risks.

> A wholly privatized, largely deregulated health care market is toxic to entrepreneurialism because of these risks.

Except that the American health insurance market is both regulated in the extreme and, in the case of the extremely poor and the elderly, heavily subsidized by taxpayers as Medicaid/Medicare. I really don't know what the effects of a private, deregulated health insurance market would be because we're so far from that.

I think there may be good arguments for either free market health care or nationalized health care. But whatever this thing that we've got is, it should be burned to the ground.

> 2b. Continuity of coverage may itself be at risk with pre-existing conditions returning to the political debate.

This reminds me, when I was in college I had a pretty bad accident, but I had some college provided health care plan my parents paid for that covered it.

Even after being employed and having employer health care, I kept renewing it incase I had a longer term issue related to the accident that my new insurance wouldn't cover due to it being pre-existing.

In particular, I had to get a rod inserted into my leg, and thought if I had a problem with it down the line, it might get denied by my new insurer.

If you or your dependents have any medical complications or are something other than young and healthy, the costs can increase drastically. Also employers often provide a lot of resources via HR and FAQ websites for navigating health care related topics. And I think there is safety in numbers so to speak. Insurance companies don't care at all if they loose one customer. They care a lot if they loose a big contract with a big company. Maybe they'll decide you provided false information in one of their 1,000 forms and thus will deny coverage when you desperately need it. They're less likely to pull that sort of crap if you can complain to your employer and have them apply pressure.

Put simply: there's little incentive for health insurance companies to provide good service to individuals; there's lot of incentive to provide good coverage to company employees.

If that really is the problem then you, as a freelancer, can hire a company to navigate and negotiate the health care plans for you and other freelancers as a pool and get the same quality and discounts as you would in a large corporation.

But even so, they'll be a middle-man and they'll try to take as much profit from the group discounts they get instead of passing those savings on. An employer doesn't have an incentive to make profit there.

I don't know, do they? If they do, then your premise is correct and there's enough benefit in negotiating in groups that it's worthwhile. If there aren't, then it's either a) the "economist sees a 20 on the ground and immediately assumes it's fake because someone else would have picked it up otherwise" or b) your premise is wrong and having a large HR department doesn't make a difference in your plan costs and pricing.

The real answer is that they do exist. I used Oscar for a year and their plans were actually by either United Healthcare or Aetna (I don't remember anymore) and the premiums were less and the quality was identical to what I had through a company provided insurance later. There's also Justworks that does something similar, though they're more of a full HR service provider.

There are so many fewer options when you're not a larger company with group healthcare buying power. A middle class family of 4, to get the worst healthcare available on the marketplace (i.e. 7k deductible/max per person, very limited doctors) may pay 1300/mo from what I've seen (more than doubled from a couple years ago). Large employer subsidized healthcare from places like Aetna give better rates but don't offer individual plans ([0] "we don't offer individual health plans at this time").

Not OP, but have had to buy insurance as a freelancer before.

Do you have a family? Health insurance prices are far, far higher if you have a family.

The type of coverage you can by as an individual is also inferior to those you get access to at large companies, so it can be harder to get in-network coverage.

I agree. I have been independent for almost two decades and paid for my family’s health insurance all that time. If you factor in the cost in your planning, there isn’t any reason for it to be a big deal. At least no more than housing, or car insurance or any of the basic, predictable expenses.

One issue is you have to pay a monthly. In most other countries you wouldn't have to do this, so you dont have to worry if you have a slow month, or no work at all.

I have made career moves that I couldn't have made if my employment was the source of my family's healthcare. When it comes to actual "freedoms" this is a big one.

As a single income parent, I'd probably not be seeking out employment that I was passionate about, and would stick with what's safe.

Glad to see this as a top comment. So frikin true in the USA. When I started my freelance/contracting business, the first thing that came to mind was "oh shit, how will I manage Health Insurance". The fear factor is huge.

While we pay above average for top tier talent on Upwork, it still makes me wonder how Freelancers cover their healthcare costs (if at all?).

The Freelancer Union, mentioned in the article, seems like a good start. Could they collectively pool funds to get high-deductible coverage for ~$200 per month?

At age 33, I pay 30 USD per month for 100% coverage of any illness, up to 30,000 USD per year, which is enough even for cancer. That's in Hong Kong.

The only problem is American prices. Socialized healthcare is not needed as long as prices are reasonable.

If I was an American I'd probably just fly to Thailand for any serious health issues because the cost of flight ticket plus treatment would be significantly less than in the US.

For most people, that may work, but for many with chronic conditions, most of their cost is medicine to maintain their health, not treatment. (and some medicines could blow through that $30k cap quickly)

Warning. If you do get sick with cancer do not travel to the US. 2 DAYS in the Emergency room could cost 30k. You would be setup for immediate bankruptcy.

Simply because insurance corporations have shareholders to serve. There's just no incentive for insurers to lower prices.

It's the nature of corporations to maximize profit. That can be a good thing, but not when health and lives are at stake, which is something that lower class conservatives don't understand the economics of, and upper class business owners profit off of. It's an ugly emergent property of the system we've built.

> "If I was an American I'd probably just fly to Thailand for any serious health issues because the cost of flight ticket plus treatment would be significantly less than in the US."

What you're describing is called "medical tourism" and it is slowly becoming more popular in the USA but still a fairly niche and underground idea.

I cover my healthcare costs by adding it into my bill rate. Same way I pay for every other employee benefit I don't get as a contractor (like vacation, disability, 401k match, software/hardware, SE Tax, etc).

If you are wondering how they cover their healthcare costs then your 'above average' must not be very much. My US insurance was subsidized due to low income but it still cost $300 per month, with the medication and fees the total was over $400.

How is that going to help? It's the cost of healthcare that matters, not the universal system. Unless you mean that salaried workers should foot the bill for freelancers who have unpredictable income streams. That is neither sustainable nor fair.

Universal systems in fact can be a hindrance to freelancers. They are expensive, making it hard to make the first step, and the result is people go illegal or underreport their income.

At least health insurance is a problem you can solve with money. There are going to be a lot harder problems that you can't directly solve with money as a freelancer/entrepreneur. If health insurance is your main barrier to entry then you're probably not cut out for it to begin with.

To make the discourse more useful, could you give some examples of what you believe to be harder problems and why they're harder than health insurance (ie, why cant they too be solved with money, and why is money such an "easy" solution?)

Money is an easy solution because you can get a job and make money. And you can live below your means and build a savings. And if you choose to freelance or start a business at some point you can use that savings to get yourself started.

As far as hard vs easy problems, health insurance is relatively easy because, for the most part, if you buy a reputable health insurance plan you're good. Obviously there's horror stories of people not getting the coverage they believe they paid for but generally it works as advertised. An example of a more difficult problem would be finding clients/customers. Even though you can pay money for leads/ads/content writers etc. you are not guaranteed a good client or customer. You can't directly pay for a good client or customer. You can directly pay for things that are likely to lead to good clients or customers but you are still going to have to work.

You can basically sign up for health insurance online and as long as you pay the bill there's no work involved. If you're setting out to WORK for yourself, and something that takes no work is stopping you, you don't really have the right attitude.

This assumed that it is easy to get a job that pays enough above living expenses for the leftover money to be enough for health insurance. If getting such a job is hard, I'd argue that the money that ensues from said job would be hard too.

Agreed that if getting a job is hard then getting the money that ensues is hard. But for the vast majority of people getting a job and living below your means is possible. Does that mean it's necessarily going to be a comfortable lifestyle? Maybe not. But it is possible. And if your goal is to start your own business you should expect some sacrifices.

Offtopic from your post for a couple paragraphs: I push back against my fellow conservatives who view things like basic living income a "socialist" idea. It seems to me that if people have more money in their pocket, they will buy more--good for capitalism.

Also, if they have at least a minimal safety net and are not endangering their family, home, and bellies they will seek out work that is more fulfilling to them and therefore perform better.

Maybe it's because I work in the healthcare industry, but I don't see universal healthcare as having the same safety-net effect. Other than stabilizing prices, it would only be a situation where the healthy support the sick. That is not inherently a bad thing, but needs to be recognized that way.

> I don't see universal healthcare as having the same safety-net effect.

Why not? People work shit jobs solely for health insurance. People need healthcare and will do demeaning, exploitative things to get it. We should aim to decrease exploitation of people and having something along the lines of Medicare for all or single payer insurance would accomplish that goal.

> Other than stabilizing prices, it would only be a situation where the healthy support the sick.

Sounds like insurance. Mutual aid ought be a founding principle of any society.

> Mutual aid ought be a founding principle of any society.

The fact that the US has the same principles already in place (MedicAid, MediCare, veterans...) shows that it is not a matter of your society's helpfulness but a matter of your society's institutions that block reform out of self-interest.

Pre-ACA, I was denied coverage at 30 with a wife and kid, with no pre-existing conditions and from the same companies I had health insurance from when working fulltime. This was in 2011, it was scary and I felt the system was broken. I was healthy and had no idea why it happened, both BCBS, Aetna and other large private insurers hate individuals and small companies because they group by company not across everyone and individuals are riskier to them with that system. Aetna and BCBS are employer focused rather than individual/consumer focused.

Post-ACA pre-existing conditions are covered and everyone has to be approved for coverage, breaking healthcare from employers as the customer and making them focus on consumers is key and ACA started that movement and better private markets even if it was a rocky start.

Healthcare is the riskiest part of freelancing/contracting and now at least you can get it guaranteed with ACA.

If we removed it from employers entirely and made individuals/families the customers rather than get it through the job, it would help people change jobs, start businesses, travel, reduce ageism and allow us to compete better with countries that do have single payer/universal or healthcare not attached to employers over consumers, it may also fix pricing when it is closer to the consumer or there is a public Medicare for all option for competition that the individual can choose.

Employers don't want to pay for healthcare and people shouldn't want employers knowing their private health, nor choosing the service for them. Employers don't get your auto or home insurance, nor should they, why healthcare?

Private insurance or public options like Medicare for all will make business easier and healthcare more consumer focused, it is a pro-business way to set it up, right now we have anti-business healthcare legacy systems and it is making US companies less competitive because they are expected to offer it. They can pay more for employees to go get their own, they don't need to choose and manage it. That will also help reduce the 'real compensation' parasitic leech that healthcare costs are hiding under, sucking up raises and wage increases into 'real compensation' for healthcare benefits rather than actual wage increases.

Ok, we can agree to disagree on morality it is more about a broken focus in essentially a scam system with the focus on employers and insurers not paying when time comes, rather than a focus on individuals/consumers and larger more sensible grouping of covered people to spread risk and not have insurance rates spike for entrepreneurs, small businesses or people with pre-existing conditions. Employers shouldn't have anything to do with providing healthcare or deciding/choosing for you, making people have to change insurance to change jobs and people losing insurance if they do need it as employers and insurers drop you if that happens.

At a macro level, everyone would be served better by healthcare where the consumer/individual is the customer focused on, not some deal with large employers where they are the customer. That current setup in healthcare purposefully tries to exclude people who are individuals, smaller businesses or other due to broken grouping that insurers use. We'd be better served by large groups across all ages, conditions and states, that would truly be insurance, more like auto insurance which is not bound to employers.

We don't get our auto or home insurance from employers. Why do we get the most private of insurance, healthcare, from employers? It is a legacy broken system that most of the world has moved on from. Benefits are one thing, pay is another, but healthcare should not be provided by employers as it leads to broken fixed pricing between large insurers, medical suppliers and the consumer is considered last if at all, leading to the worst pricing fixed market maybe in history. If you support entrepreneurs and small business growth, the engine of America, you'll come around.

Unless those freelancers/entrepreneurs happen to have any kind of health history what so ever. In that case they'd have to stick with a large employer group plan.

Fun fact: in 2011 nearly half of the US population had a preexisting condition that would have affected pre-ACA medical underwriting.

Absolutely not. Pre-ACA options were heavily biased to healthy, young individuals.

This is not the profile of freelancers and entrepreneurs, and especially not the profile of the most qualified contributors to an entrepreneurial market.

As you get older, you get more experienced and better networked, which can yield the best opportunities for freelancing and entrepreneurialism. But you also accumulate dependents, medical conditions, and risks of the sams. All of thess were grossly penalized pre-ACA, to the point that many would-be entrepreneurs and freelancers wouldn’t be eligible for coverage at all.

I'd say biased to mostly healthy, not-old individuals and I would say it's a reasonable profile for most. At the least, not "absolutely not". What makes one qualified or more valuable is a different discussion as is morality.

It's not that binary. Strict rules on insurers essentially means shared. Shared by law requires trust in government spending, something there is little of and the spending is volatile per cycle.

It is binary. Pre-ACA options might have been cheaper because sick people weren't in the pool. If you want to cover old and sick people, then you have to pay more. Doesn't matter if it's taxpayers paying or taxpayers paying via insurance premiums, it has to come out of someone's pocket.

Most of that is not true if you recognize costs are as much of a problem as distribution. When you only target recipients/insurers/payers instead of the providers with these rules, it sure can seem like the only option is to have most people pay more. And then treating that as the only way, stating it as fact, and making the discussion binary limits true solutions to these problems from even being discussed.

Insurance premiums when people with pre-existing conditions were not covered are lower than when people with pre-existing conditions are forced to be covered. That statement would be true no matter how much providers are getting paid.

Lack of supply of providers or fraudulent billing by providers is a separate cause of increased insurance premiums, but I don't see what ACA has to do that, and if anything, healthcare spending increases are slowing down since the passage of ACA, and premiums are even decreasing in many parts of the country.

My original response was to your claim that freelancers were better off in pre-ACA times, to which I wanted to point out that was only because people with pre-existing conditions were denied insurance. Nothing in ACA has caused the amount paid to providers to increase.

Unless you have a preexisting condition. Yeah, it's expensive now, but it's a much more improved situation when the insurance companies can't say no (and the alternatives that have been proposed, like high risk pools, have so far been trash in terms of quality of lifetime care compared to current status quo)

How do you figure? Please elaborate on this. I don't see how subsidized premiums and guaranteed coverage would be a detriment to freelancers... Yes, the cost of healthcare was cheaper back then, but it likely would have risen more without ACA.

Your last sentence is pure speculation. There was never an equivalent rise. The spike is due, in part, by the ACA’d requirements that covered more than the original plans covered. Some of use didn’t want to cover those costs. When I priced a plan before ACA, $300 family of two. Closest plan after $750. I didn’t qualify for credits. So I had two mortgage payments:650 for house 750 for medical. SMH.

Obamacare exploded the cost. It’s hollow succor to say the rocketing costs are accelerating less. All your supposed evidence shows is that the markets are getting worse. The ACA is plagued by dine and dashers. https://johnhcochrane.blogspot.com/2018/06/aca-dropouts.html

{kind=link}

{kind=link}